On 22 June, Volodymyr Zelenskyy signed a record budget of 4.4 trillion hryvnia ($97.6 billion), most of it borrowed from Europe. The money to keep Ukraine fighting, and eventually to rebuild it, is flowing as never before.

The constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

That same quarter, the economy it is meant to revive posted its sharpest contraction since the wartime recovery began—and the constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

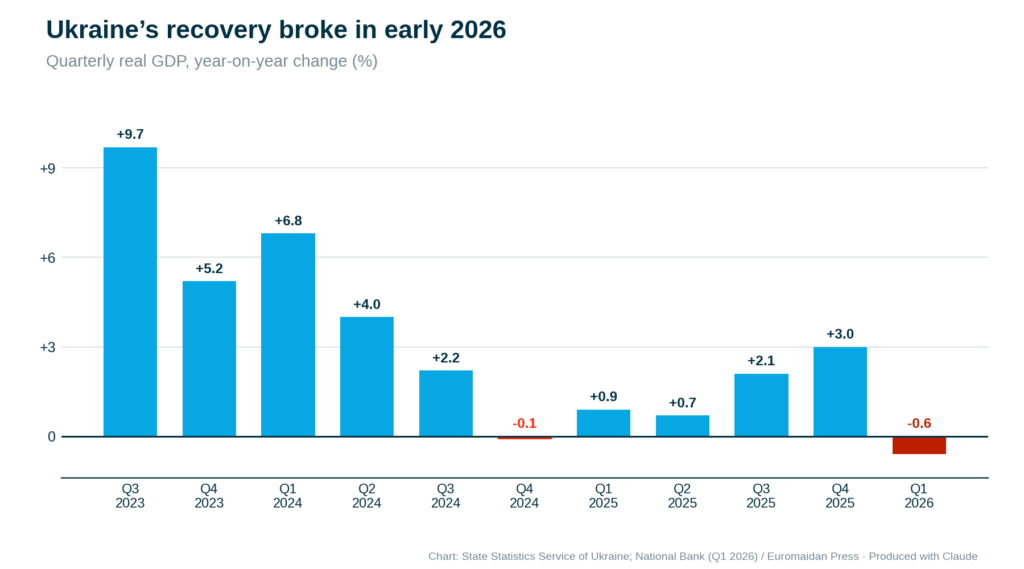

Real GDP fell 0.6% year-on-year in the first quarter of 2026, the National Bank confirmed on 18 June, and 0.7% against the previous quarter. The number is small. What hides behind it is not.

For nearly three years, Ukraine’s economy grew through bombardment—near-continuously from the middle of 2023, when the country clawed its way back from a collapse of almost 29% in the invasion year. It dipped only once before now, briefly, when drought hammered the harvest at the end of 2024. The first quarter of 2026 was the sharper break.

The investment house ICU said it bluntly: weak growth is “the new norm.”

It is the sharpest contraction since the recovery began, and the forecasters who first called it a winter blip have spent the spring marking the year down: the National Bank to 1.3%, the IMF to between 1 and 1.6%. The investment house ICU said it bluntly: weak growth, its analysts wrote, is “the new norm.”

The official line is more hopeful: the National Bank expects growth back as soon as the second quarter, and the government pencils in 4.5% for 2027. But a bounce off a depressed quarter is not a recovery, and the full-year number has only been marked down further.

Where the bombs show up in the accounts

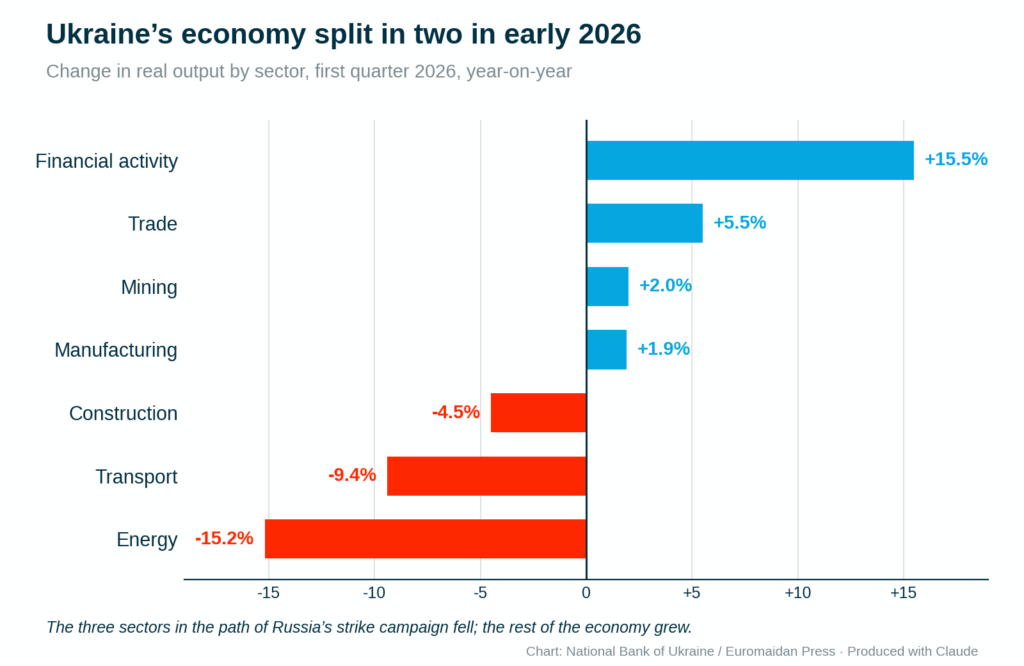

The contraction has a clear author. Energy output fell 15.2% year-on-year, transport 9.4%, and construction 4.5%, the National Bank’s breakdown showed—the sectors directly in the path of the strike campaign, now showing up as line items in the national accounts.

The economy contracted because three bombed sectors outweighed a domestic economy that kept working.

The first sector to fall was electricity generation, with transmission disrupted where the grid was hit; the second was transport, after heavy strikes on the railways, economist Oleksandra Betliy told Kyiv Post.

Household consumption rose 11%. Manufacturing grew 1.9%, trade 5.5%, financial activity 15.5%, and mining 2%. The economy contracted because three bombed sectors outweighed a domestic economy that, by almost every other measure, kept working. ICU called the quarter a display of “unprecedented resilience” to the blackouts.

The hryvnia keeps sliding

Unlike the contraction, the hryvnia’s slide owes nothing to the weather. Through the first five months of 2026, the hryvnia weakened against the National Bank’s official rate—from a 2025 average of 41.7 to the dollar to 42.9 in January, 44.1 by May, and 44.9 by 23 June. A widening trade gap drives the slide, the Centre for Economic Strategy reported.

A cold snap can knock out a quarter of GDP growth. It cannot make a currency depreciate every month for half a year. That slide tracks a structural deficit between what Ukraine earns abroad and what it spends there, and it will outlast the spring.

Reserves dropped to $45.7 billion by the start of June.

Defending that slide has cost the central bank its cushion. Reserves dropped to $45.7 billion by the start of June, down from a record near $57.7 billion early in the year—roughly $12 billion sold off in four months to slow the hryvnia while partner aid ran late. The National Bank calls the level sufficient, about 4.7 months of imports, and the inflows now arriving are meant to refill it.

Prices, at least, are easing. Inflation slowed to 8.2% in May, helped by falling oil prices as the war in the Middle East de-escalated—Washington cleared Iranian crude sales on 22 June, pushing prices to around $74 a barrel, which both cheapens Ukraine’s energy imports and thins Russia’s war revenue. The National Bank held its key rate at 15% on 18 June, judging the easing cycle done for now.

The deeper drag

The contraction had near-term authors—the strikes, the cold, the delayed budget spending. The drag beneath them is older, and no thaw fixes it: Ukraine is running out of people. The number of full-time employees fell from 7 million in 2021 to 5.3 million by late 2025, according to GMK Center, citing official data.

The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%.

Half of companies were already citing the staff shortage as the main obstacle to their businesses six months ago, Euromaidan Press reported, citing the National Bank’s enterprise survey, and the labor force has only thinned since then.

The war took around a quarter of the labor force; 5.9 million Ukrainians are abroad; and the National Bank expects the net outflow to run into 2027 before any return begins. The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%, and a large part of why every forecaster now caps growth near zero.

Money is arriving

For most of the war, the binding question was whether the money would come at all. In February, it nearly didn’t: Hungary’s Viktor Orbán blocked the €90 billion ($104 billion) EU loan agreed in December, holding it hostage to a dispute over Russian oil through the Druzhba pipeline.

Then Orbán lost his election after 16 years; his successor dropped the obstruction; the pipeline was repaired; and the bloc finally approved the package on 23 April—€45 billion ($52 billion) of it for 2026.

The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP.

That money is what funds the record defense budget. The first €3.2 billion ($3.7 billion) tranche of budget support lands at the Recovery Conference in Gdańsk on 25–26 June, with €5.9 billion ($6.8 billion) for the army to follow by the end of the month, European Pravda reported.

The central bank expects roughly $13 billion in June across all programs. The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP, from the 18.5% first planned, the Centre for Economic Strategy noted in the same review, though defense spending is running at only about 80% of plan, and the budget underfunded the military pay raises it promised.

The bind is no longer the money

The bill, as of December 2025, is almost $588 billion—nearly three times the country’s annual output—a joint assessment estimated by the World Bank, EU, and UN in February, up from the $524 billion figure of a year earlier.

$20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap.

To rebuild and keep pace with its neighbors, Ukraine needs around $40 billion a year, the Berkeley economists Yuriy Gorodnichenko and Maurice Obstfeld estimate: $20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap. Set against Poland’s post-communist investment inflows, or the immobilized Russian assets sitting in Europe, that figure is not a fantasy.

The problem is the other side of the ledger. Ukraine can realistically absorb $10 to 15 billion a year right now, Ukraine’s deputy representative at the IMF, Vladyslav Rashkovan, argued on a Centre for Economic Strategy podcast.

If $100 billion arrived this month, he said, the country could not spend it. Not enough projects are ready. Not enough institutions to run them. Not enough throughput at a customs service that would have to clear 10 times the imports.

The question now is whether Ukraine can build the capacity to take the funding.

The workers to do the rebuilding are scarcer still: around 4.5 million will be needed, the Economy Ministry projected already in January, in an economy already short more than 600,000 skilled hands this year.

The constraint has quietly flipped. For three years, the question was whether the world would fund Ukraine. The question now is whether Ukraine can build the capacity to take the funding—and that is slower, less photogenic work than wiring a loan.

It is also the work that decides everything downstream. Investment does not go where a president points it, Rashkovan said; it goes where the balance of risk and return beats the alternatives. The institutions, the rule of law, the energy capacity to power a rebuilt economy, the workers to build it—none of it visible, all of it now the binding constraint on whether the recovery resumes or settles into the new normal ICU described.

Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains.

The contraction may not be the most important number from this June. Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains. The bombs are still landing on the sectors that fell. And the hryvnia, indifferent to the weather, keeps closing on 45.

Read also

-

What does Russia do when sanctions strand ten ice-class tankers? It offers to buy them

-

Russia’s biggest oil company stopped selling gasoline in canisters nationwide after Ukraine’s strikes. It blames “seasonal demand”

-

Russia quietly lets refiners sell lower-grade Euro-3 fuel as drone strikes squeeze supply